Choosing the right financing option is crucial for tech companies looking to scale their operations, invest in innovation, or maintain cash flow. Two common funding options are venture debt and traditional bank loans. While both provide capital, they serve different purposes, have distinct requirements, and impact your business in unique ways. This guide will help you understand the key differences between venture debt and bank loans, their pros and cons, and how to decide which is the best option for your tech company in 2025.

Understanding Venture Debt and Bank Loans

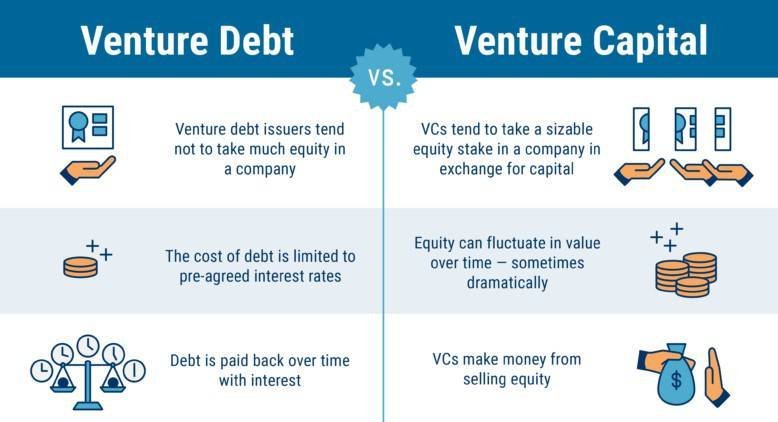

What is Venture Debt?

Venture debt is a form of financing designed for startups and growth-stage companies that have already received venture capital (VC) funding. It provides additional capital without requiring the company to give up more equity.

- Best for: Startups with strong growth potential.

- Loan Amount: Typically $1 million to $10 million.

- Repayment Terms: Shorter repayment periods (2-5 years).

- Requirements: Backing from a venture capital firm.

What is a Bank Loan?

Bank loans are traditional debt financing provided by banks and financial institutions. They require companies to have strong financial records, credit history, and collateral.

- Best for: Established tech companies with stable revenue.

- Loan Amount: Varies, but typically $500,000 to $5 million+.

- Repayment Terms: Longer repayment periods (5-10 years).

- Requirements: Good credit, collateral, and financial history.

Key Differences Between Venture Debt and Bank Loans

| Feature | Venture Debt | Bank Loan |

|---|---|---|

| Equity Dilution | No equity loss | No equity loss |

| Risk Level | Higher risk due to shorter terms | Lower risk with structured payments |

| Approval Speed | Faster approval process | Longer approval process |

| Collateral Required | Often unsecured or IP-backed | Requires collateral or personal guarantee |

| Interest Rates | Higher than bank loans | Lower, fixed, or variable rates |

Pros and Cons of Venture Debt

Pros

- No equity dilution, allowing founders to retain control.

- Faster approval process than traditional bank loans.

- Useful for funding between VC rounds.

- Can be used to extend runway or fund R&D.

Cons

- Higher interest rates compared to traditional loans.

- Shorter repayment terms, requiring faster payback.

- Often requires venture capital backing.

- Risk of financial strain if growth projections are not met.

Pros and Cons of Bank Loans

Pros

- Lower interest rates than venture debt.

- Longer repayment terms provide financial stability.

- No requirement for venture capital investment.

- More predictable monthly payments.

Cons

- Requires strong financial history and collateral.

- Longer application and approval process.

- May require a personal guarantee from business owners.

- Less flexibility in loan use compared to venture debt.

Which Option is Best for Your Tech Company?

Choose Venture Debt If:

- Your company is a startup or growth-stage business backed by venture capital.

- You need quick access to capital to extend your cash runway.

- You want to avoid further equity dilution.

- You have strong projected revenue growth and can manage short-term repayment.

Choose a Bank Loan If:

- Your company has an established revenue stream and solid financial records.

- You are looking for long-term, low-interest financing.

- You have collateral or strong credit to secure the loan.

- You prefer a stable repayment schedule with lower risk.

Alternative Financing Options for Tech Companies

If neither venture debt nor bank loans are the right fit, consider these alternative funding options:

1. Revenue-Based Financing

- Best for: Startups with steady revenue streams.

- Repayments are based on a percentage of future revenue.

- No collateral or equity required.

2. Government Grants and SBA Loans

- Best for: Small tech businesses needing support.

- SBA 7(a) and 504 loans offer lower interest rates and long repayment terms.

- Non-repayable grants available for R&D and innovation.

3. Convertible Notes

- Best for: Early-stage startups.

- A loan that converts into equity at a future funding round.

- Delays valuation negotiations while securing capital.

Steps to Secure the Right Loan for Your Tech Business

Step 1: Assess Your Business Needs

- Identify how much capital you need and what it will be used for.

- Determine your ability to repay within the loan’s terms.

Step 2: Review Financial Health

- Ensure your credit score and financial records are strong.

- If seeking a bank loan, prepare collateral documentation.

Step 3: Compare Lenders and Loan Terms

- Evaluate venture debt providers vs. traditional banks.

- Compare interest rates, repayment schedules, and requirements.

Step 4: Prepare a Strong Loan Application

- Include a detailed business plan and revenue projections.

- Showcase how the funds will drive growth and ensure repayment.

Step 5: Negotiate Terms and Finalize Agreement

- If taking venture debt, clarify any warrants or equity-linked terms.

- For bank loans, negotiate the best possible interest rate and term length.

Future Trends in Tech Financing

1. AI-Powered Loan Decisions

- Banks and venture lenders are using AI to streamline loan approvals.

- Automated risk assessments reduce processing times.

2. Growth of Alternative Lenders

- Online lenders and fintech platforms offer flexible financing for tech companies.

- Revenue-based and blockchain lending solutions are gaining traction.

3. Increased Government Support

- More government-backed loan programs for tech startups.

- Expansion of low-interest financing options to support innovation.

Conclusion

Choosing between venture debt and bank loans depends on your tech company’s stage, financial health, and funding goals. Venture debt is ideal for fast-growing startups looking to extend their runway without giving up more equity, while bank loans offer a stable, lower-cost financing option for established businesses. By carefully evaluating your needs and exploring alternative funding sources, you can secure the best financing solution to drive your tech company’s growth in 2025 and beyond.